Your bank is paying you 0.39%. The best high yield savings 6% 2026 seekers are earning more than 10 times that — and the only thing stopping most people is not knowing where to look.

Published: April 2026 | Reading Time: 20 minutes | Category: Personal Finance & Saving

IMPORTANT DISCLAIMER: This is informational content. All APY rates cited in this post are verified from live sources as of April 2026. High-yield savings account rates are variable and can change at any time in response to Federal Reserve decisions and individual bank policy. Always verify the current rate directly with the institution before opening an account. This post is for informational purposes only and does not constitute financial advice. All accounts mentioned are FDIC or NCUA insured up to $250,000 per depositor.

Let’s start with a number that should make you genuinely angry.

The FDIC’s reported national average for savings account APY as of March 2026 is 0.39%.

That means if you have $20,000 sitting in a standard savings account at Chase, Bank of America, or Wells Fargo, you are earning approximately $78 a year in interest. That’s $6.50 a month. For the privilege of lending your bank twenty thousand dollars, they are paying you the cost of a single oat milk latte per month.

Meanwhile, the best high-yield savings accounts available right now are paying up to 5.00% APY — fully FDIC-insured, zero risk, zero market exposure, and often with no fees and no minimum balance.

On that same $20,000, 5.00% APY earns you $1,000 a year. The difference between what your bank is paying you and what the best online banks and credit unions are paying is $922 every single year. On your savings. That are already sitting there. Doing nothing.

This post is your complete guide to the best HYSA over 5% APY available right now — including the accounts, the rates, the fine print, the credit union secrets, the fintech options your bank definitely doesn’t want you to know about, and the strategy for keeping your emergency fund at 6% APY even as the Fed continues adjusting rates.

Let’s get into it.

Why Are Banks Still Paying You 0.39% in 2026?

Before we get to the accounts, it’s worth understanding why this gap exists — because understanding it makes you angry in a productive way.

Traditional banks — the big brick-and-mortar institutions with branches on every corner — have enormous overhead costs. They’re paying for real estate in every city, thousands of tellers and branch managers, legacy IT infrastructure, and marketing budgets that run into the billions. All of that overhead has to be funded somehow, and one of the primary ways it’s funded is by underpaying you on your deposits.

Traditional banks run branch networks and offer everything under the sun — loans, checking, credit cards, you name it. High-yield providers are usually online-only, keep their offerings lean, and have no physical locations to maintain. That operational simplicity translates to better rates for you.

That’s the mechanism. The big banks are not offering you 0.39% because they can’t afford to pay more. They’re offering you 0.39% because they’ve calculated that most of their customers won’t leave. Inertia, brand familiarity, and the minor friction of switching accounts combine to keep hundreds of millions of dollars in low-yield accounts indefinitely.

The online banks and fintech platforms on this list have made a different bet: attract deposits with high yields, keep costs low by staying digital-only, and win the customers the big banks have been quietly taking advantage of for decades.

You’re about to be one of those customers.

The Rate Reality Check: What’s Actually Available in April 2026

Before we dive into individual accounts, let’s set accurate expectations based on current market data.

As of April 2026, the top high-yield savings accounts are paying up to 5.00% APY — more than 10 times higher than the FDIC-reported national average of 0.39%. This is genuinely extraordinary when you consider that this money sits in an FDIC-insured account with no market risk whatsoever.

Here’s what the market actually looks like right now by tier:

The 5%+ Club (Conditional/Capped):

- Varo Bank — up to 5.00% APY (on first $5,000, with qualifying requirements)

The 4%+ Premium Tier:

- Axos Bank ONE Bundle — up to 4.21% APY

- Newtek Bank — up to 4.20% APY

- Wealthfront — up to 4.20% APY

- EverBank Performance Savings — competitive rate, no minimum

The Solid 3.5%–4% Tier (Established Names):

- Marcus by Goldman Sachs — 3.65% APY

- CIT Bank Platinum Savings — 3.75% APY (on $5,000+)

- Synchrony High Yield Savings — 3.50% APY

- SoFi Savings — up to 4.00% APY (with direct deposit + promo)

- Capital One 360 Performance Savings — 3.20% APY

- Ally Bank — competitive, consistently above 3%

What happened to 6%? We’ll address that directly — and honestly — in a dedicated section below. But first, let’s go deep on each of the major accounts.

You can’t fund a 6% account with a leaky budget.

High-yield savings are the engine, but your cash flow is the fuel. Most people miss out on these hidden 2026 rates because their capital is tied up in “ghost” subscriptions and banking fees.

I’m giving you my Audit Quick-Start Bundle for FREE. Use the Audit Calculator to find the hidden leaks in your accounts today so you can maximize your deposits into these high-yield winners.

[Get Your Free Audit Bundle]

The Top Accounts Broken Down: What You Need to Know

1. VARO BANK — Up to 5.00% APY

The headline rate leader for balances under $5,000

Once qualified, you can earn 5.00% APY on up to $5,000. That’s $250 a year. And any additional amount will earn 2.50%.

Varo is the most accessible route to genuinely high-yield savings right now, but it comes with qualifying conditions you must understand before opening an account.

To qualify for the 5.00% APY: To qualify for the elevated savings rate of 5.00% APY on your first $5,000, you must receive direct deposit(s) totaling $1,000 or more, and end the month with a positive balance in both your Varo Bank and Savings Accounts.

The math on Varo: At 5.00% on $5,000, you earn $250/year on the capped amount. Balances above $5,000 earn 2.50%, which is still substantially better than most traditional banks.

The real effective rate calculation: If you have $10,000 total in Varo, your blended rate is approximately 3.75% — still excellent, but significantly below the advertised 5.00%. At balances above $8,333, SoFi Bank earns more due to Varo Bank’s APY cap.

Best for: Anyone with a balance under $5,000, or who wants the highest possible rate on their emergency fund’s first tier while keeping larger savings elsewhere.

FDIC insured: Yes. No monthly fee. No minimum opening deposit.

2. AXOS BANK ONE BUNDLE — Up to 4.21% APY

Best for larger balances needing one high rate across the board

The Axos ONE® bundle makes your money work overtime — all under one roof. Meet the direct deposit and balance requirements, and you’ll earn up to 4.21% APY on savings and up to 0.51% APY on checking. There are no physical branches, but you can still access cash easily through a network of over 95,000 fee-free ATMs.

Qualifying requirements: To receive the promotional APY, the Axos ONE® Checking account must receive monthly qualifying direct deposits of at least $1,500 in total, and the average daily balance must be at least $1,500.

Why Axos wins on larger balances: While Varo’s 5.00% is capped at $5,000, Axos’s 4.21% applies to balances up to $499,999.99. At balances above $7,310, Axos Bank earns more due to Varo Bank’s APY cap.

Without the bundle: Axos also offers a Summit Savings account at 3.75% APY with no bundling or direct deposit requirement — a solid no-fuss option.

Best for: Savers with balances significantly above $5,000 who want a single high-yield account without multiple institutions.

FDIC insured: Yes. No monthly maintenance fees.

3. SOFI SAVINGS — Up to 4.00% APY

Best overall digital bank experience

In 2026, SoFi® Bank, N.A. won NerdWallet’s annual award for best overall bank. Its SoFi Checking and Savings earns an APY of 3.30% on the savings portion. To earn that rate, you’ll need to set up direct deposit, deposit a total of at least $5,000 every 31 days, or be a SoFi Plus member.

The current promotional rate brings SoFi to around 4.00% APY for qualifying members — making it extremely competitive for anyone who can meet the direct deposit requirement.

The promo rate caveat: SoFi Bank’s 4.00% rate includes a promotional bonus for the first 6 months, after which it reverts to the standard rate (currently 3.30%). Set a calendar reminder for month 5 to reassess whether switching makes sense.

What makes SoFi genuinely excellent beyond the rate: The combined checking and savings experience is polished, the app is superb, and SoFi regularly offers sign-up bonuses for new direct deposit customers — sometimes $50–$400 depending on the promotion.

Best for: Young professionals who want a complete digital banking relationship with competitive savings rates and a checking account under one roof.

FDIC insured: Yes. No monthly fees.

MARCUS BY GOLDMAN SACHS — 3.65% APY

Best no-fuss, no-requirements HYSA from a brand name you trust

The Marcus Online Savings Account is backed by Goldman Sachs and comes in with 3.65% APY. The savings account offers no minimum opening deposit and comes with no monthly fees.

Marcus is the definition of “set it and forget it.” No qualifying requirements, no direct deposit needed, no balance tiers, no monthly fee, no minimum. You put money in, and it earns 3.65% APY. Full stop.

There is no limit to the number of withdrawals or transfers you can make from your online account. Your account must be funded within 60 days of opening to avoid closure.

The Goldman Sachs backstop: For savers who are slightly nervous about fintech institutions, Marcus carries the Goldman Sachs brand and regulatory standing — about as reassuring a backstory as any online bank can offer.

Best for: Anyone who wants a reliable, no-maintenance HYSA without jumping through hoops. Ideal for an emergency fund you want to set up and not think about.

FDIC insured: Yes. Zero fees. Zero minimums.

CIT BANK PLATINUM SAVINGS — 3.75% APY (on $5,000+)

Best for savers with established emergency fund balances

CIT’s Platinum Savings account pays 3.75% APY on balances of $5,000 or more. If your balance dips below $5,000, it earns a paltry 0.25% APY.

This tiered structure is both CIT’s greatest feature and its biggest risk. If you consistently maintain over $5,000 — which is reasonable for a funded emergency fund — you get one of the best unconditional rates available. If your balance fluctuates below $5,000, the rate cliff is severe.

CIT Bank also runs periodic APY Boost promotions: accounts enrolled in the Platinum Savings APY Boost promotion will receive a 0.35% APY boost on the current standard APY tiers for 6 months. This can temporarily push the rate above 4.10% APY — one of the strongest promotional offers available.

Best for: Established savers with a consistent $5,000+ balance who want reliability without direct deposit requirements.

FDIC insured: Yes. No monthly fee. $100 minimum opening deposit.

SYNCHRONY HIGH YIELD SAVINGS — 3.50% APY

Best for ATM access alongside online savings

With the Synchrony High Yield Savings account, you’ll earn a solid 3.50% APY on all balances. There are no minimum requirements and no monthly maintenance fees. Synchrony doesn’t charge ATM withdrawal fees itself, but there may be fees associated with using a certain ATM. However, account holders can get up to $5 in domestic ATM fee reimbursements per month.

Synchrony’s value proposition is straightforward: a clean, flat rate on all balances with no strings attached, plus an ATM card — something many HYSAs don’t offer. For people who occasionally need physical cash access from their savings, Synchrony solves a real friction point.

Best for: Savers who want a no-fuss HYSA with the ability to access funds via ATM.

FDIC insured: Yes. No fees. No minimum.

CAPITAL ONE 360 PERFORMANCE SAVINGS — 3.20% APY

Best hybrid option for those who want branch access

The 3.20% APY attributed to the 360 Performance Savings account is competitive. The account also has no monthly fees and doesn’t require a minimum balance. Capital One provides customer service seven days a week.

Capital One occupies a unique space: it’s genuinely digital-first, but it also has a physical branch and café presence across major cities. For savers who occasionally want in-person banking but still want above-average yields, the 360 Performance Savings is a strong hybrid choice.

The app consistently rates above 4.6 stars on Android and 4.9 on Apple’s App Store — among the best in class.

Best for: Anyone who values brand familiarity, physical access, and a no-fee high-yield account without wanting to go fully fintech.

FDIC insured: Yes. No fee. No minimum.

DISCOVER ONLINE SAVINGS — Competitive 2026 Rate

Best for customers who want card rewards + savings under one roof

Discover Online Savings continues to be one of the most recognized names in the HYSA space for 2026. Discover’s advantage has always been the combination of no-fee, no-minimum savings with the ability to pair it with one of the most rewarded cash-back cards in the market — letting rewards from spending flow directly into a high-yield account.

Discover is consistently listed among the top HYSA options by NerdWallet, Bankrate, and CNBC Select. Always check current rates at discover.com/online-banking/savings before opening, as rates adjust regularly.

Best for: Existing Discover card holders who want a seamless rewards-to-savings pipeline.

FDIC insured: Yes. No fee. No minimum.

ALLY BANK — Consistently Competitive

Best for long-term reliability and ecosystem

The APY of Ally’s Savings Account is more than 5x the national average of 0.39%.

Ally has been one of the most reliable names in online banking for over a decade. It may not always have the absolute highest rate at any given moment, but it has a track record of keeping rates competitive, a genuinely excellent app, and a full suite of savings tools including “savings buckets” that let you virtually divide your savings by goal — emergency fund, vacation, car replacement — within a single account.

For savers who value stability and banking relationship quality alongside rate, Ally is a perennial top choice.

Best for: Long-term savers who want a complete digital banking relationship they can grow into.

FDIC insured: Yes. No fee. No minimum.

BREAD SAVINGS — Strong CD Rates and Solid HYSA

Best for CD laddering alongside your HYSA

Bread Savings is an online bank that offers a solid high-yield savings account with a $100 minimum opening deposit. There’s no monthly fee. You can also open CDs with Bread, many of which earn great rates.

Bread Savings shines particularly for savers who want to pair a competitive HYSA with a CD ladder strategy. Their CD rates are regularly among the top in the market, and managing both products on the same platform makes the CD ladder vs HYSA 2026 decision easy to act on.

Best for: Savers with more than 3–6 months of expenses saved who want to optimise with a CD ladder while keeping liquid savings in a competitive HYSA.

FDIC insured: Yes. No monthly fee. $100 minimum opening deposit.

The 6% Question: Is a “Hidden 6% Bank Account” Actually Real?

Let’s address the elephant in the room directly — because financial content online is full of misleading claims about hidden 6% bank accounts, and you deserve an honest answer.

The straightforward truth as of April 2026: A standard, unconditional high-yield savings account paying 6% APY on a major, widely available platform does not currently exist in the U.S. market. The Fed’s benchmark rate sits at 3.50%–3.75% following several cuts in late 2025, and that ceiling limits what even the most aggressive online banks can sustainably offer on liquid savings.

Where rates approaching or exceeding 5–6% do exist in specific circumstances:

1. Promotional / Introductory Rates Some institutions offer time-limited introductory rates. CIT Bank’s APY Boost promotion has pushed the Platinum Savings rate toward 4.10%+ for 6-month periods. SoFi’s promotional rate for new direct deposit customers has reached 4.00%+. These are real, legitimate rates — but they expire.

2. Qualifying / Conditional Rates with Hard Caps Varo’s 5.00% rate is genuine — but it applies only to the first $5,000 and requires monthly qualifying direct deposits. This is the closest thing to a “hidden 6% bank account” in the current market: a real rate that’s significantly above what most people know exists, but with conditions that filter out most casual savers.

3. Credit Union High Interest Savings — The Real Hidden Gem This is where the genuinely under-publicised rates live. Consumers Credit Union (CCU), for example, offers up to 5.00% APY on checking account balances up to $10,000. Connexus Credit Union and other member-owned institutions regularly match or beat major online banks — sometimes significantly. Credit union high interest savings rates are often not included in mainstream comparison sites, which is why they feel “hidden” to most savers.

4. Fintech Savings with Behavioural Requirements Some fintech platforms structure their highest rates around spending or saving behaviours. APYs 4.5%+ crush inflation. Online banks dominate. Zero fees mandatory. Shop weekly — rates flux. The trick is finding which conditions you can realistically meet and calculating your actual effective yield, not just the headline number.

The bottom line on “6% savings accounts”: The closest real-world equivalent is a stack of strategies: Varo’s 5.00% on the first $5,000 of your emergency fund, combined with a competitive HYSA for the balance, potentially layered with a short-term CD for the portion you won’t need for 6–12 months. The effective blended yield on a well-structured savings stack can meaningfully exceed 4.5% in the current market — not 6%, but dramatically better than what your bank is currently paying you.

The Credit Union High Interest Savings Secret

The most underutilised sector of the HYSA market is credit unions — and it’s underutilised specifically because credit unions don’t have billion-dollar marketing budgets.

Credit Union Shoutout: Alliant Credit Union hits 4.6% APY. Member-owned perks. ATM card. 300K+ free ATMs. Travel-friendly.

Credit unions are member-owned financial cooperatives — which means that instead of paying profits to shareholders, they return value to members in the form of better rates, lower fees, and more flexible lending. For savers, this translates directly into higher APYs.

Key credit unions worth investigating in 2026:

- Alliant Credit Union — consistently among the top credit union HYSA rates; membership is broadly accessible via a simple joining fee to a qualifying organisation

- Consumers Credit Union (CCU) — up to 5.00% APY on qualifying checking balances up to $10,000; one of the most competitive rates in the entire market when requirements are met

- Connexus Credit Union — competitive rates with straightforward membership eligibility

- Lake Michigan Credit Union — Max Checking account earning competitive APY available to members nationally

How to join a credit union: Most credit unions that offer competitive savings rates have broadened their membership eligibility. Alliant, for example, is open to anyone who makes a small donation to its partner charity. Many are nationally accessible online despite their community credit union origins.

NCUA protection: All federally insured credit union accounts are protected by the NCUA (National Credit Union Administration) to the same $250,000 per depositor limit as FDIC protection. Credit union accounts are not less safe than bank accounts.

Rate Drop Protection: How to Safeguard Your Yield When the Fed Cuts Again

Here is one of the most important — and least discussed — aspects of the HYSA space in 2026: rate drop protection strategy.

All variable-rate savings accounts can reduce their APY at any time. During the last three meetings in 2025, the Fed made cut after cut to the federal funds rate. The Fed’s last two meetings, including the latest on March 18, 2026, brought no change to the current 3.50%–3.75% rate. It’s likely your high-yield savings account’s APY will remain the same for the time being — but financial institutions can still adjust rates for reasons not tied to Fed actions.

The practical implication: the rate you open an account with today is not guaranteed tomorrow.

The rate drop protection playbook:

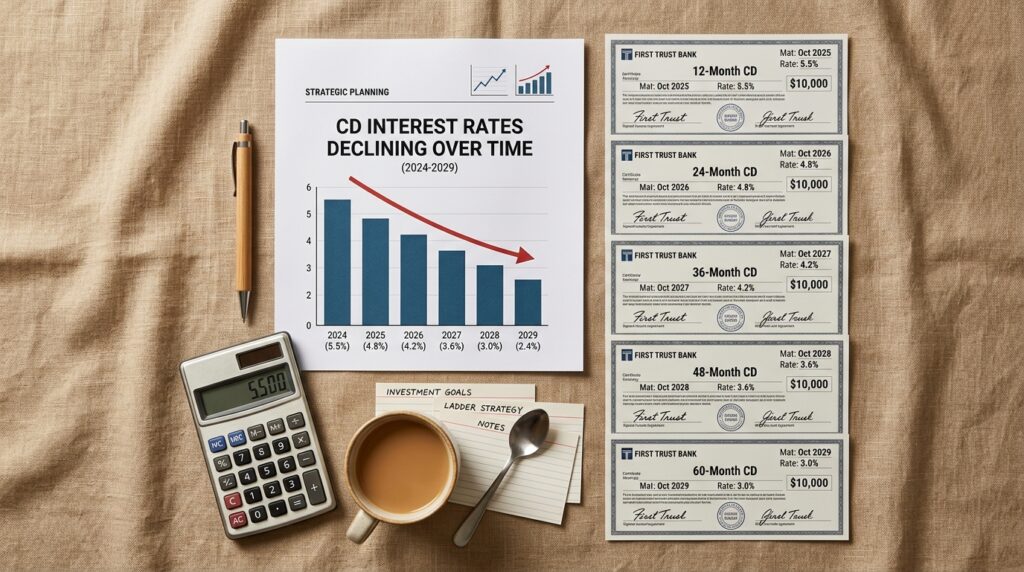

Strategy 1 — The CD Ladder Lock a portion of your savings in CDs at today’s rates. CDs are worth considering if you can afford to lock your money away for a set period of time. A simple CD ladder — dividing your savings into three equal portions in 3-month, 6-month, and 12-month CDs — gives you both rate protection and regular liquidity windows.

With 12-month CDs from institutions like Bread Savings or CIT Bank currently offering rates above 4.20%, locking in this rate protects you from any mid-year rate cuts.

Strategy 2 — The HYSA Rotation Monitor your current HYSA rate quarterly against the market. Sites like Bankrate and NerdWallet publish daily rate updates. When your current provider drops their rate by more than 0.25%, begin the process of moving to the current market leader. The inconvenience of switching is typically outweighed by the rate differential within a few months.

Strategy 3 — The Emergency Fund Floor Keep your emergency fund (3–6 months of expenses) in a HYSA with no conditions and no lock-in. Keep any savings above the emergency fund threshold in CDs, Treasury bills, or money market funds for better long-term yield. This creates a natural tiered structure where your most critical liquid savings stay accessible and your surplus savings earn higher returns.

Strategy 4 — CD Ladder vs HYSA 2026 Decision Framework

- If you won’t need the money for 12+ months: favour CDs at today’s rates

- If you might need the money within 12 months: HYSA with the highest unconditional rate

- If you can meet qualifying requirements: Varo for the first $5,000, then a no-condition HYSA for the remainder

Building Your Emergency Fund at 5% APY: The Step-by-Step Guide

An emergency fund at 6% APY — or realistically, 4.5–5% APY in the current market — changes the psychological and financial calculus of an emergency fund entirely.

At 0.39% (the national average), a $15,000 emergency fund earns $58.50 a year. It feels like money asleep. At 5.00% APY (Varo on the first $5,000), 4.21% (Axos on the remainder), your $15,000 emergency fund earns roughly $560–$600 a year — money that is actively covering part of its own maintenance.

How to structure a tiered emergency fund for maximum yield:

Tier 1 — $0 to $5,000: Varo Bank at 5.00% APY Open a Varo Bank Account and Savings Account. Set up your qualifying direct deposit of $1,000+/month. This tier of your emergency fund earns the market’s best liquid rate. The key condition — maintaining direct deposits — is met as a natural byproduct of your existing payroll setup.

Tier 2 — $5,000 to $20,000+: Axos ONE or Marcus For balances above Varo’s $5,000 cap, move to either Axos ONE (4.21% APY, requires $1,500 direct deposit/balance) or Marcus by Goldman Sachs (3.65% APY, zero requirements). Choose Axos if you can meet the requirements; Marcus if you want zero friction.

Tier 3 — Savings above your emergency fund: CD Ladder Any savings beyond your 6-month emergency fund target should be working harder than a HYSA. A simple 12-month CD at 4.20%+ (Bread Savings, CIT, or equivalent) locks in today’s rate and earns meaningfully more than the best HYSA on funds you won’t need for at least a year.

Fintech Savings Platforms: The No-Minimum 5%+ Options

Beyond the established online banks, a growing class of fintech savings platforms offers competitive and sometimes leading rates with genuinely minimal friction:

Wealthfront Cash Account — ~4.20% APY Wealthfront, primarily known as a robo-investing platform, offers a Cash Account that competes directly with the best HYSAs. No minimum balance, no fees, FDIC-insured through partner banks. The advantage for Wealthfront users: seamless movement between the Cash Account (high-yield savings) and investment accounts.

EverBank Performance Savings — Competitive APY, No Minimum EverBank Performance Savings is great for maximising the interest you earn through a high-yield savings account. This account has no minimums required or monthly fees. EverBank’s rate is among the most consistently competitive in the market.

Newtek Bank — 4.20% APY, No Minimum A quieter name in the HYSA market, Newtek Bank Personal High Yield Savings won NerdWallet’s 2026 Best-Of Award. The account has no minimum to open, no monthly fee and earns a 4.20% APY — one of the highest rates around. This is the definition of a “hidden” high-yield account — strong rate, no conditions, FDIC-insured, and almost no mainstream marketing.

LendingClub LevelUp Savings — Competitive APY LendingClub’s LevelUp savings account pays a higher yield when you deposit at least $250 monthly into the account, though you’ll still earn a competitive yield if you don’t meet this requirement. The behavioural requirement here — adding $250/month — is actually a feature for disciplined savers, as it rewards the savings behaviour you should be practising anyway.

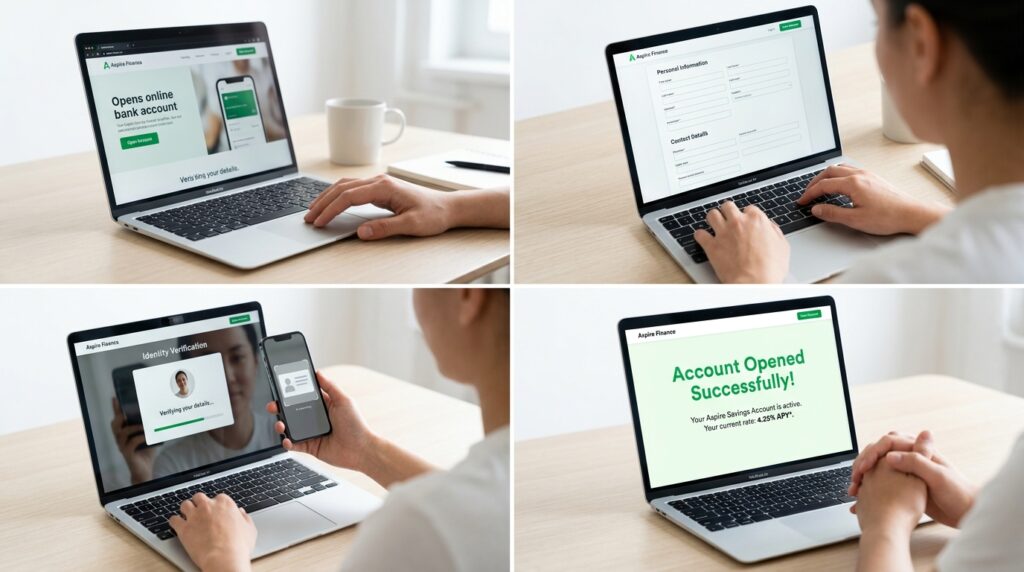

The Practical Switching Guide: How to Move Your Money in 48 Hours

If you’ve been sitting on a 0.01%–0.39% savings account and you’re ready to act, here is the exact process to switch to a high-yield account:

Step 1 — Choose your account (15 minutes) Use the guide above to match your situation to the right account:

- Balance under $5,000 + can meet direct deposit requirement → Varo

- Balance above $7,000 + can meet direct deposit requirement → Axos ONE

- Want zero requirements, medium rate → Marcus by Goldman Sachs

- Want to investigate credit unions → Alliant Credit Union or Consumers Credit Union

- Want a rate-plus-CD strategy → Bread Savings or CIT Bank

Step 2 — Open the account online (10–15 minutes) All accounts listed in this post can be opened entirely online. You’ll need: your Social Security number, government-issued ID, current bank account details for the initial transfer, and a phone number for verification.

Step 3 — Fund with an initial transfer (immediate, funds move in 1–3 business days) Link your existing bank account via ACH and initiate the transfer. Most online banks allow you to start earning interest from the day of the transfer request.

Step 4 — Update your direct deposit (if required) For Varo and Axos, update your direct deposit through your employer’s HR portal or payroll system. This typically takes one pay cycle to take effect.

Step 5 — Keep $1 in your old account Don’t close your old account immediately. Automated payments, linked accounts, and tax documents may still reference it. Keep a nominal balance for 60–90 days while you verify nothing is still routing through it.

Step 6 — Set up automatic savings transfers Most HYSAs have automatic transfer features. Set a recurring monthly transfer from your checking account to your new HYSA to continue building your balance systematically.

The Numbers: What 5% APY Actually Means Over Time

The interest rate conversation often gets reduced to monthly interest comparisons. The more compelling frame is the compound interest picture over 3–5 years.

| Balance | 0.39% (Big Bank) | 3.65% (Marcus) | 5.00% (Varo, first $5K) | Annual Difference |

|---|---|---|---|---|

| $5,000 | $19.50/year | $182.50/year | $250.00/year | +$230.50 vs big bank |

| $10,000 | $39/year | $365/year | ~$375/year (blended) | +$336/year |

| $20,000 | $78/year | $730/year | ~$730/year (blended) | +$652/year |

| $50,000 | $195/year | $1,825/year | ~$1,850/year (tiered) | +$1,655/year |

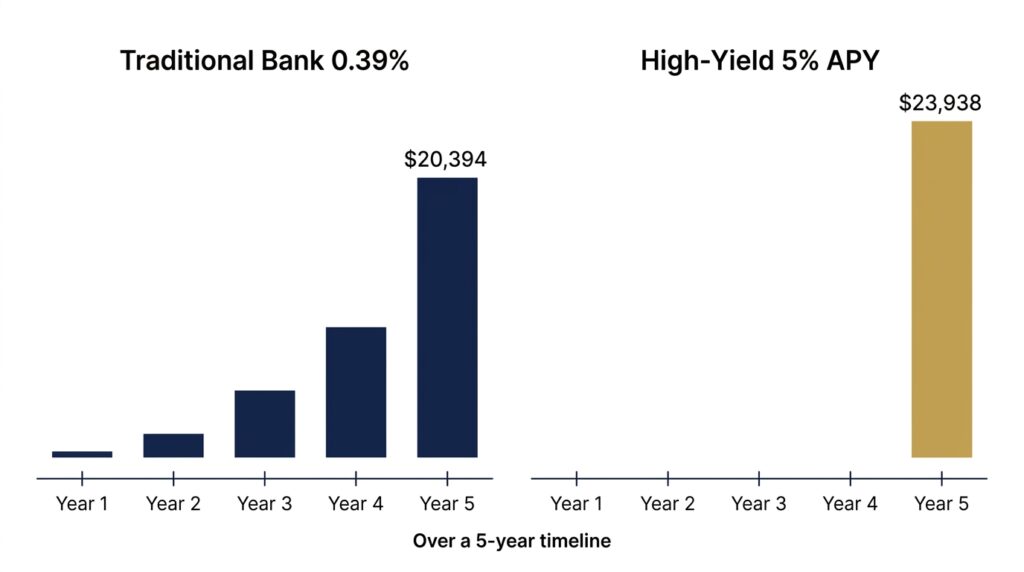

Over five years, with monthly compounding, a $20,000 balance at 3.65% APY (Marcus) grows to approximately $23,938 — compared to just $20,394 at the national average 0.39%. That’s a difference of over $3,500 on money that is already sitting in savings, doing nothing, in a completely risk-free account.

Common HYSA Mistakes to Avoid in 2026

Mistake 1 — Chasing the headline rate without reading the conditions Always calculate your actual effective APY based on your specific balance and ability to meet qualifying requirements. Varo’s 5.00% on a $50,000 balance has a meaningfully lower effective rate than its headline number.

Mistake 2 — Ignoring the rate after opening Consumers can expect to see the interest rates paid on most HYSAs decline further as the Fed continues to lower interest rates. Savers who are seeking the highest yields may need to actively monitor the interest rate they’re receiving and move their money if they’re seeking to maximise the rate. Set a quarterly calendar reminder to check your current rate against the market.

Mistake 3 — Keeping all savings in one account above $250,000 If your bank is insured by the FDIC or your credit union is insured by the NCUA, your savings are federally insured to at least $250,000. It’s important to confirm that the savings account you select is federally insured. If your total savings exceed $250,000, spread them across multiple institutions to maximise FDIC/NCUA protection.

Mistake 4 — Treating a HYSA as a long-term investment strategy Other investment options offer better returns. In the past 10 years, the S&P 500 has had an average annual return of 12.39%. An APY of 5% in a high-yield savings account doesn’t compare as favourably. A HYSA is for your emergency fund, short-term savings goals, and cash you’ll need within 12 months. Money earmarked for 5+ year horizons should be in diversified investments.

Mistake 5 — Leaving money in a low-yield account because switching feels complicated The entire opening process for any account on this list takes under 20 minutes. The interest differential on even $10,000 at 5.00% vs 0.39% is over $460 per year. You have now spent more time reading this article than it will take to open a better account.

FAQ: Everything You Still Want to Know

Are high-yield savings accounts safe in 2026? Yes. Every account in this post carries either FDIC (for banks) or NCUA (for credit unions) insurance up to $250,000 per depositor per institution. Your principal is fully protected regardless of market conditions. This is categorically different from investments.

Do I pay tax on HYSA interest? Yes. Interest earned in a high-yield savings account is taxable as ordinary income. The interest earned in a HYSA is taxable income. You should receive a Form 1099-INT from your bank if you earn more than $10 in interest during the year.

What happens to HYSA rates if the Fed cuts rates again? HYSA rates are variable and typically move in correlation with the federal funds rate. Banks and credit unions have applied withdrawal and rate changes unevenly in practice — some maintain higher rates longer than others to remain competitive. Rate monitoring and periodic switching between providers is the best hedge against rate declines.

Is there really no catch with no-fee, no-minimum HYSAs? For genuinely fee-free, no-minimum accounts like Marcus and EverBank, the answer is essentially no — there is no hidden catch. The business model is sustainable because online banks use customer deposits to fund loans at higher interest rates than they pay depositors, keeping the spread as profit.

Can I have more than one HYSA? Yes, and for larger savings pools, it’s actively smart — both for FDIC protection diversification and for taking advantage of different platforms’ promotional rates simultaneously.

Final Thoughts: The Real Hidden Savings Account Is the One You’re Not Using Yet

The concept of “hidden 6% bank accounts” that banks hate is, at its core, a framing device for a genuinely important truth: the vast majority of people with savings accounts are earning dramatically less than they could be, and the barrier to change is almost entirely psychological rather than practical.

The accounts in this post are not exotic financial instruments. They are not risky. They are not complicated to open or use. They are straightforward, FDIC-insured savings accounts offered by legitimate institutions that have simply chosen to compete on rate rather than rely on customer inertia.

The best high-yield savings accounts in April 2026 offer APYs up to 5.00%, far higher than the national average, helping you grow your money faster with minimal risk. Top accounts typically feature low or no minimum balance requirements and minimal fees, making them accessible and cost-effective.

Your emergency fund at 5% APY versus 0.39% APY is worth hundreds to thousands of dollars per year in additional interest — money that compounds, year after year, into a meaningfully larger safety net.

That is not a hack. That is not a trick. That is simply paying attention.

The best time to switch was when these rates first went up. The second best time is today.

Did this post help you find a better savings account? Share it with someone whose money is still sitting at 0.39%. And bookmark this page — we update rate information regularly as the market changes.

Don’t just find a better bank—build a Wealth Command Centre.

Moving your money to a hidden 6% account is a high-yield move, but as a Wealth Strategist, I know that true financial freedom requires a complete command centre to manage the flow. I managed my own “Wealth Shift” into these top-tier 2026 accounts using the 6-in-1 Professional Engine Room.

Command your capital with the full suite:

- Professional Invoice Generator: The high-precision system I use to bill clients for the service income that funds my high-yield investments.

- Ghost Audit Tracker (Spreadsheet): Automatically identify and “exorcise” the phantom fees and subscriptions that the big banks hope you never notice.

- Daily Revenue & Expense Tracker: The CPA-grade precision tool for logging your interest gains and every dollar of business income.

- Notion Command Centre: Your central digital vault for banking strategies, exit plans, and tax-ready documentation.

- Wealth Shift PDF: My strategic manual for outperforming traditional “low-spread” banking in 2026.

- The Audit Blueprint: The roadmap to transforming your messy data into a clean, profitable wealth engine.

[Get the 6-in-1 Engine Room – Secure Your 6% Future]

Rates Disclosure: All APY rates cited in this article were verified from live sources including Bankrate, NerdWallet, Fortune, CNBC Select, The Motley Fool, and direct bank websites as of April 2026. Rates are variable and subject to change without notice. Always verify current rates directly with the institution before opening an account. This article is for informational purposes only and does not constitute financial advice. Consult a qualified financial advisor for guidance specific to your situation.